Weekly Recap

It’s been another wild week in financial markets, bringing Q3 to a close with a blistering end-of-season finale.

This week’s main story was the huge GBP volatility as the pound continued to tank at the start of the week, extending losses from the prior Friday’s UK mini-budget. Traders reacted aggressively to the tax cuts and spending announced and the implied plans to increase UK public borrowing. GBPUSD fells to its lowest level on record along with wild swings against JPY and EUR.

UK yields soaring to multi-year highs forced the BOE to step in and announce an emergency £65 billion bond-buying program. Subsequently, the downside move found massive demand into the lows seeing GBP reverse ferociously higher, almost erasing losses by the end of the week. The driver behind the reversal was partly expectations of aggressive rate hikes to come from the BOE as well as speculation that the UK government might reduce the spending outlined in the mini-budget, leading to less borrowing.

Equities tanked across the week as GBP volatility highlighted growing concerns for the health of the global economy. Rising bond yields kept the pressure on equities across the week, leading to a tech meltdown in the US as leading names like Apple and Tesla broke to fresh monthly lows.

The deliberate explosion of the Nord Stream pipelines between Russia and Germany added to weak investor sentiment as fears of nuclear war rose. On Friday, Russia officially annexed the four regions of Ukraine that held referendums on joining Russia across the week.

The latest round of Eurozone inflation data showed that consumer prices moved further into record highs last month. With CPI still not subsiding, the market is upgrading its ECB projections for the remainder of the year with pricing now moving in favor of more than 1% of additional tightening this year, along with upside risks towards 1.5% of tightening.

The US Dollar fell from grace this week. DXY reversed lower despite a slew of hawkish Fed commentary over the week reinforcing expectations for further tightening this year. It seems that market action elsewhere has stolen the limelight from USD, at least temporarily.

Coming Up This Week

- RBA & RBNZ October Rates Meetings

The RBA & RBNZ will kick off this month’s central bank meetings. Both central banks have been firmly engaged in tightening over recent months and have issued hawkish forward guidance, putting market expectations in favor of further rate increases. Both central banks are expected to hike by a further 50bps and, given these expectations, the focus will be on guidance issued at these meetings. If both banks maintain a hawkish view, this should see AUD and NZD supported. However, if there is any sense that either bank is looking to pause or slow on tightening, this could be met with a sharp downside reaction because of the contrast with more aggressive action elsewhere.

- ECB Meeting minutes

The latest ECB meeting minutes this week could draw a great deal of attention. Given the hawkish expectations now gripping the market, traders will look for clues as to the ECB’s likely moves at its next meeting. With the central bank pushing for a larger rate hike last time around, as well as raising its inflation guidance, the minutes are likely to further cement hawkish expectations, underpinning EUR further here while possibly weighing on EUR share prices.

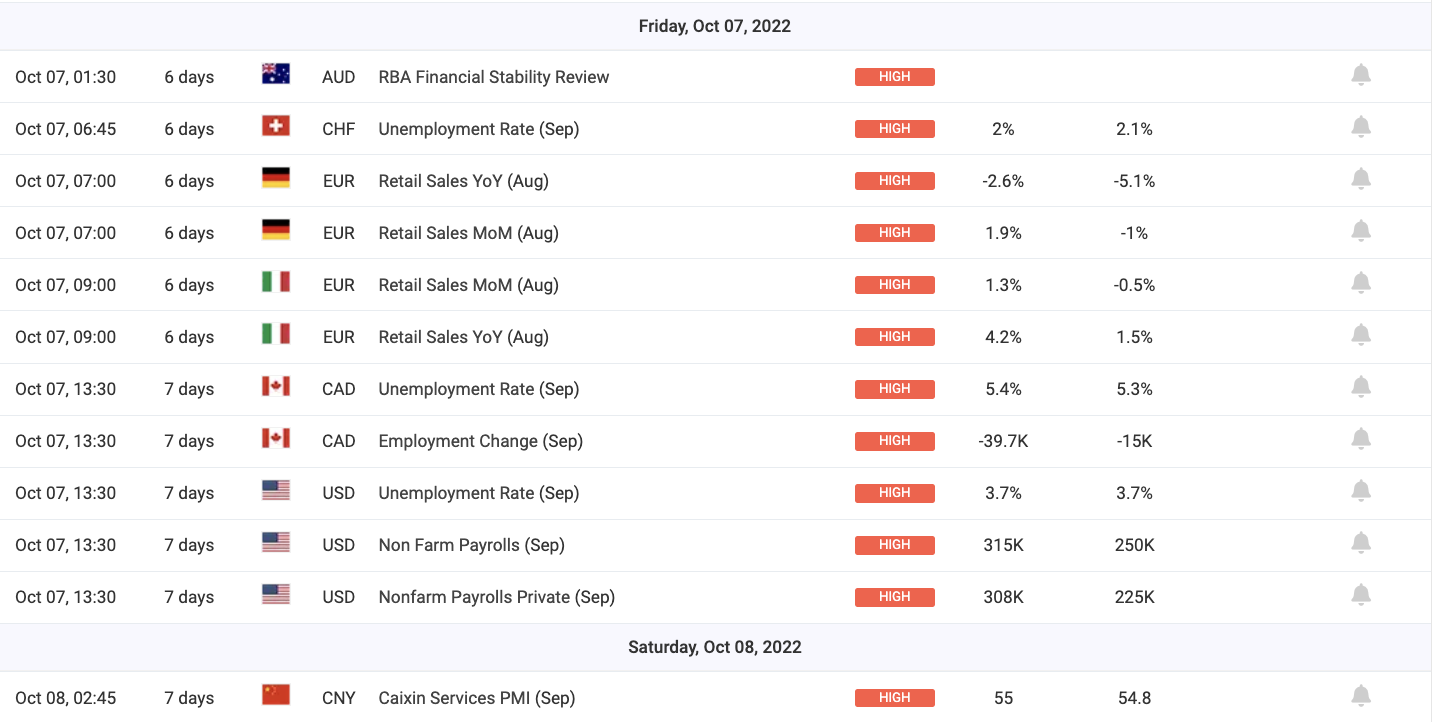

- US Labour reports – NFP, Unemployment rate, earnings

Finally, at the top of the week, there is the latest set of US labour reports. Last time around, a surprise lift in the headline NFP figure was offset by worse unemployment and earnings data. Given the recessionary concerns gripping markets currently, any issues with this latest report will likely add to the current USD pull-back. Alternatively, if data is seen improving, this should improve the near-term outlook somewhat, allowing USD to trade higher.

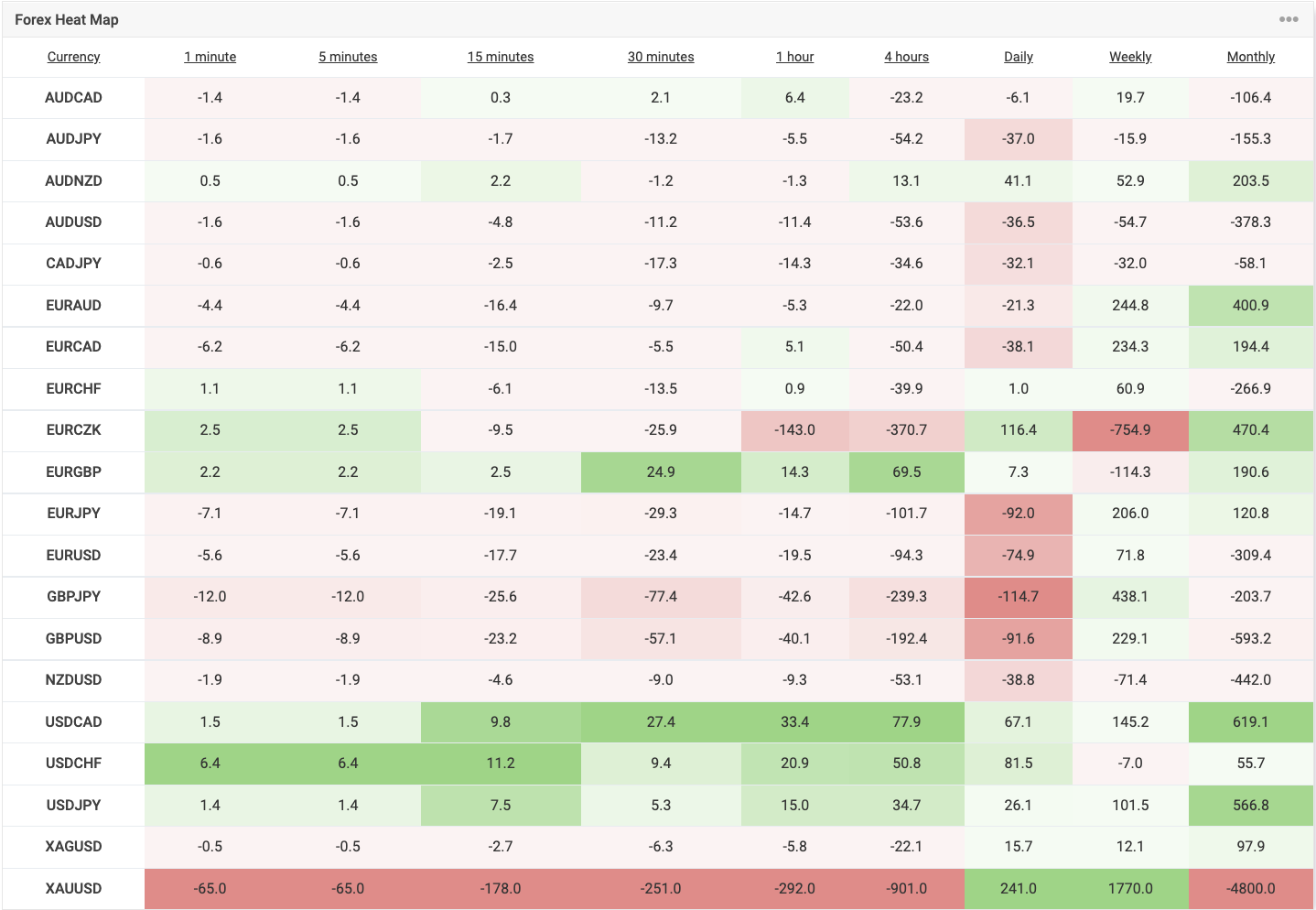

Forex Heat Map

Technical Analysis

Our favourite technical chart of the week – GBPUSD (Monthly)

The sell-off in GBPUSD this week has seen the market breaking down to fresh, record lows on the move sub- 1.05. However, the market has since bounced sharply back above that level and is now sitting back inside the bear channel which has framed price action since late 2016.

The focus now is on a further recovery higher towards the 1.2010 zone which will be pivotal for the pair. Above there, there is room for a move higher towards the channel top and 1.4150 resistance. If sellers defend that level, however, focus returns to further lows in the coming months.

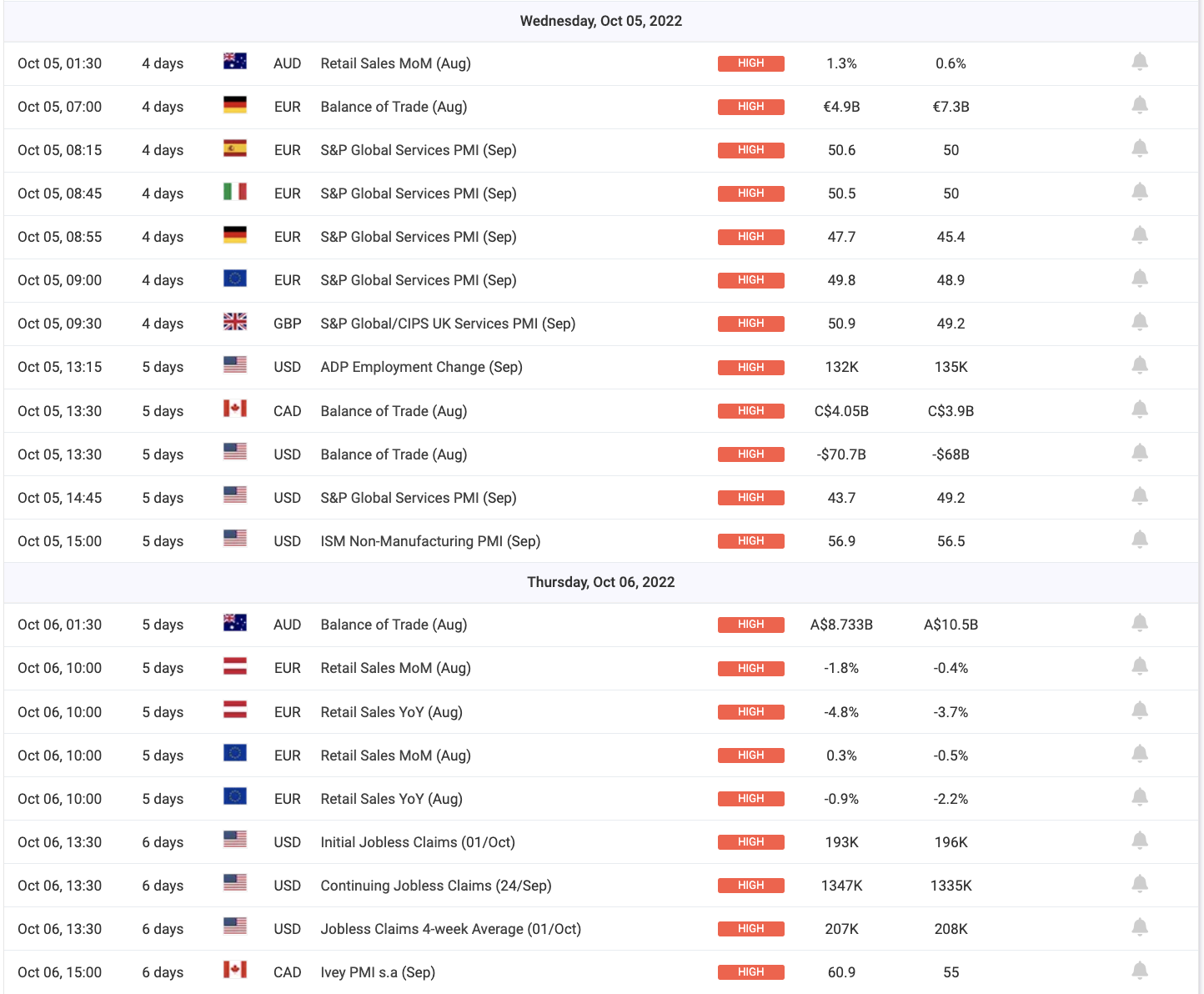

Economic Calendar

Plenty to keep an eye on this week data-wise, with the October RBA and RBNZ rates meetings along with the latest ECB meeting minutes and September NFP among other key events and releases. See the calendar below for the full schedule.

Disclaimer: This article is not investment advice or an investment recommendation and should not be considered as such. The information above is not an invitation to trade and it does not guarantee or predict future performance. The investor is solely responsible for the risk of their decisions. The analysis and commentary presented do not include any consideration of your personal investment objectives, financial circumstances, or needs.