Weekly Recap

It was a particularly busy session for traders this week with the Fed, the BOE and the RBA each holding their rate setting meetings for May. All three central banks hiked rates, adding to the wave of central bank monetary policy tightening which has dominated the landscape over recent months. However, growth fears took centre stage as the Fed and the BOE both warned of a likely downturn coming over the remainder of the year as a result of tighter monetary conditions, elevated inflation and ongoing supply-chain issues.

In the FX space, USD ended the week at highs as risk sentiment plunged amidst recessionary fears. GBP saw heavy selling across the board also on the back of the BOE’s dire outlook for the UK economy. It seems hawkish central bank expectations are now acting as a downside catalyst for respective currencies as traders anticipate slower economic activity as borrowing costs rise.

Gold prices struggled to find their footing this week. The market remains caught between risk off moves and a stronger USD which saw the safe-haven metal ending the week mid-range. While markets remain susceptible to downside shocks relating to news flow from the ongoing conflict in Ukraine, gold prices look to have a natural floor keeping them supported for now.

Oil prices ended the week at highs, shrugging off the impact of a stronger US Dollar. News mid-week that the US government is looking to buy around 60 million barrels of oil to help replenish its emergency stock created a lift in price. Reports around EU plans to ban Russian oil by 6 months-time has also added to fears over growing tightness in energy supply. Finally, OPEC+ once again pushed back against calls for faster acceleration in oil output as it stuck to its schedule of gradually unwinding production restrictions.

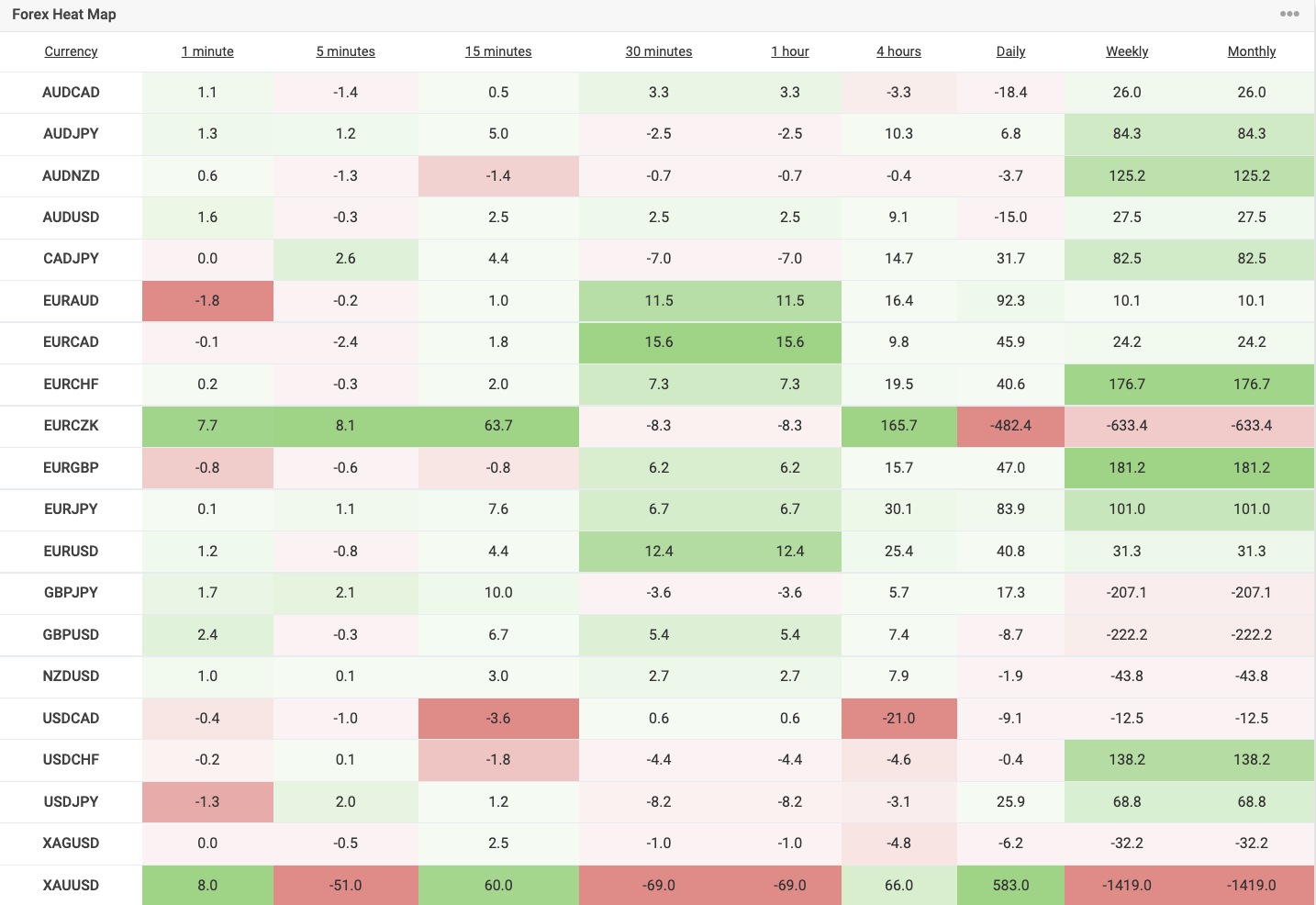

Forex Heat Map

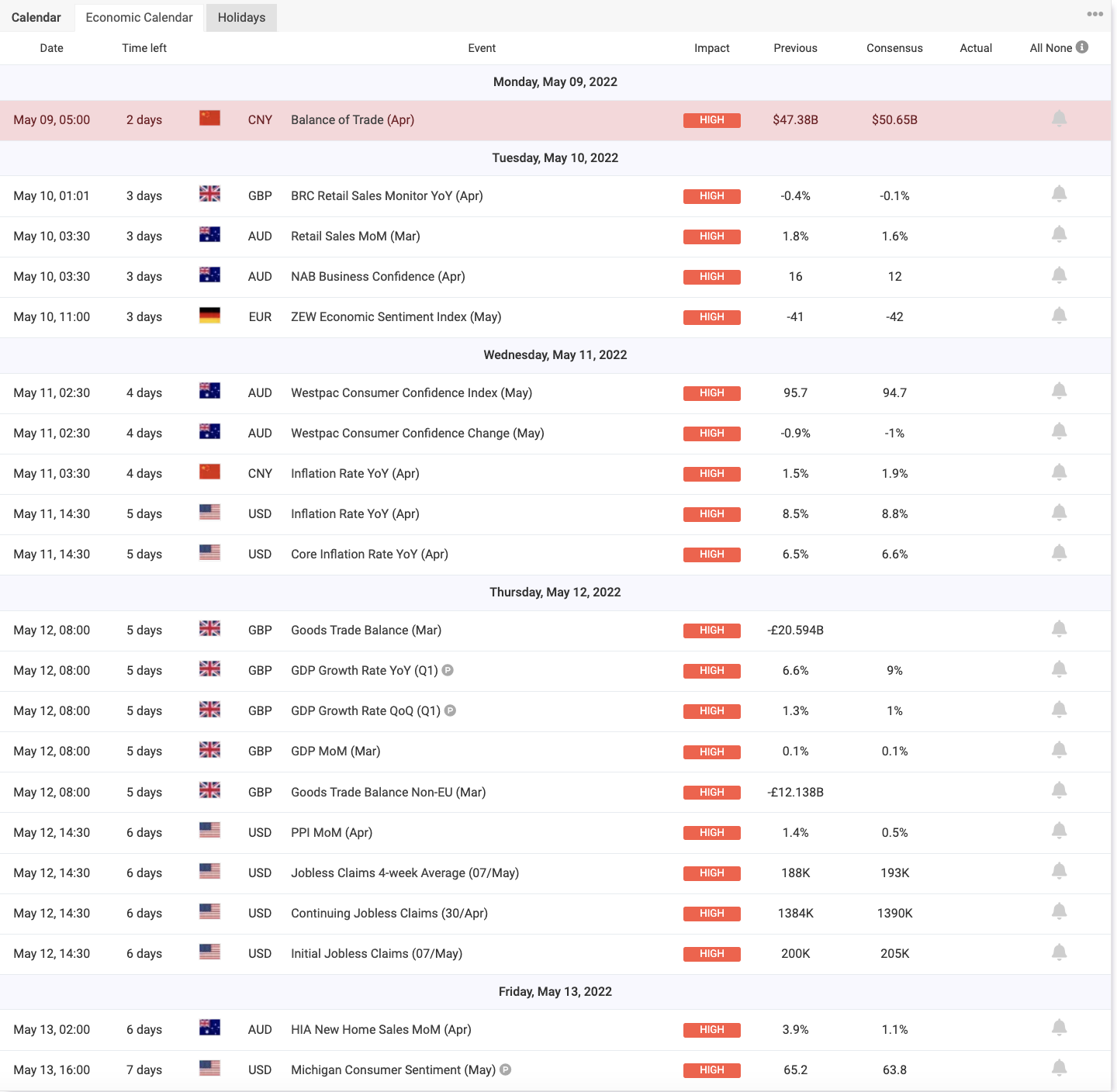

Coming up Next Week

- US CPI

Given the huge focus on soaring inflation, the upcoming CPI release will be closely watched by traders. The fed recently warned that inflation is likely to continue rising near term, warranting further .5% rate hikes. However, if inflation continues to exceed forecasts near term, traders will likely start to place greater likelihood on the Fed being forced to hike rates at a larger scale of .75%. Ahead of the May FOMC, opinions were split on whether the Fed would hike by .75%. While Powell has pushed back against larger hikes for now, continued strength in inflation might cast doubt on this position.

- UK Preliminary GDP

The first look at Q1 GDP figures in the UK will be another key focus point for traders this week. With the BOE warning over an anticipated downturn in the offing, any weakness in Q1 figures will no doubt put further pressure on GBP near-term, extending the post-BOE losses we’ve seen so far.

- US Consumer Sentiment

Consumer sentiment will round out the data sheet for the week. With energy prices soaring and inflation continuing to eat away at real incomes, consumers are likely to display concern. Consumer confidence has fallen steadily from around the 85 mark in summer last year to current lows around 65.

Technical Analysis

Our favourite chart this week is crude oil

Following the breakout above the recent contracting triangle pattern which has framed price action over the year so far, the market is now testing above the 108.94 level support. In line with the longer-term bull trend, we can look for price to continue higher while we hold above this level, putting focus on a test of bigger resistance at the 116.60 level next and 124.63 thereafter.

Crude Oil – Daily chart

Economic Calendar – High Impact

Highlights include: Australian retail sales on Monday, US & China inflation on Wednesday, UK GDP and US jobless claims on Thursday and US consumer confidence on Friday.

Disclaimer: This article is not investment advice or an investment recommendation and should not be considered as such. The information above is not an invitation to trade and it does not guarantee or predict future performance. The investor is solely responsible for the risk of their decisions. The analysis and commentary presented do not include any consideration of your personal investment objectives, financial circumstances, or needs.